The Chemical Connection: Reducing Etch System Water Usage, Part 2

The Chemical Connection: Reducing Etch System Water Usage, Part 2 It’s Only Common Sense: Nice Guys Really Can Finish First

It’s Only Common Sense: Nice Guys Really Can Finish First The Right Approach: I Hear the Train A Comin'

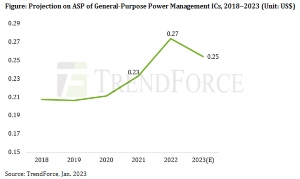

The Right Approach: I Hear the Train A Comin'Production Capacity for Power Management ICs Will Grow by 4.7% YoY for 1H23

January 6, 2023 | TrendForceEstimated reading time: 3 minutes

The effect of the low season, the planned scale-back of capital expenditure on the part of enterprises, and the ongoing slump in the wider consumer electronics market are going to constrain the demand for power management ICs during 1H23. On the supply side, Texas Instruments (TI) as the leading supplier for power management ICs will be activating the newly added production capacity at its production sites RFAB2 and LFAB in the same period. Given this circumstance, TrendForce projects that the global production capacity for power management ICs will increase by 4.7% YoY for 1H23. In the market for power management ICs, falling demand for products belonging to consumer electronics, networking devices, and industrial equipment continues to generate downward pressure on prices. Consequently, quotes for power management IC orders are projected to register a sequential drop of 5~10% during 1H23. Conversely, demand remains stable for automotive products thanks to the trend of vehicle electrification. Even though the weakening of the wider economy is causing uncertainties across the whole automotive market, prices are not expected to fluctuate significantly because of buyers and sellers of automotive products have mostly established long-term partnerships. Therefore, the demand coming from the automotive market is going to emerge as the only major driving force behind sales of power management ICs.

Major IDMs Control 63% of Power Management IC Market

Suppliers for power management ICs are diverse and include the major international IDMs as well as fabless IC design companies. Suppliers that are IDMs include TI, ADI, Infineon, Renesas, Onsemi (onsemi), STMicroelectronics (ST), and NXP. Suppliers that are fabless IC design companies include Qualcomm, MPS, MediaTek, Anpec, GMT, Leadtrend, Weltrend, Silergy, BPS, and SG Micro. By shipment market share, IDMs collectively control 63% of the global market for power management ICs; and among them, TI is the leader with a 22% global market share. TI has the advantages of having a diverse range of offerings, a consistently high product quality, and an ample amount of production capacity. Thus, it exerts an enormous influence over the global power management IC market. Looking at the general price trend of power management ICs in 2022, IDMs were able to further push up the ASP in response to rising inflation. Conversely, quotes from fabless IC design companies were first to show a weakening trend.

Suppliers Are Cutting Prices to Drive Sales of Power Management ICs for Consumer Electronics; Automotive Products and Industrial Equipment Are the Only Applications That Exhibit Stable Demand

TrendForce points out that prices of power management ICs for consumer electronics (e.g., laptop computers, tablets, TVs, and smartphones) began to drop in 3Q22, with the QoQ decline coming to 3~10%. In 4Q22, prices fell by another 5~10% QoQ for a wide range of consumer power management ICs (e.g., those related to AC-DC, DC-DC, LDO, buck, boost, PWM, and battery charger). Besides this development, demand also began to weaken for power management ICs used in networking devices and most kinds of industrial equipment. The only applications that still exhibited stable demand were a very few specific kinds of industrial equipment (e.g., military hardware) and automotive products. At that time, order visibility for these application was already extended to 2Q23. And there were no notable attempts to drive sales of related power management ICs through price cutting.

However, TrendForce also notes that IDMs together hold a market share of more than 83% for power management ICs embedded in industrial equipment and automotive products. Fabless IC design companies for the most part still have difficulties in penetrating into these particular market segments, but their efforts have been aggressive as the overall demand for consumer electronics remains depressed. Currently, fabless IC design houses are working hard to get their new automotive and industrial power management ICs qualified as soon as possible.

Regarding the lead time for power management IC orders, TrendForce’s latest investigation finds that fabless IC design houses now have an average lead time of 12~28 weeks. Moreover, existing stock is so large for some models of power management ICs that fabless IC design houses can begin shipments right after receiving the incoming order. Turning to IDMs, they still mostly have a longer lead time. For power management ICs belonging to non-automotive applications, IDMs have a lead time of 20~40 weeks. For power management ICs belonging to automotive applications, IDMs have a lead time of more than 32 weeks. On the whole, orders are still in the allocation status for automotive power management ICs that come from very few suppliers and have a drawn-out process for chip manufacturing, module assembly, and qualification.

Share on:

Suggested Items

Real Time with… IPC APEX EXPO 2024: My Role as a Technology Solutions Director

05/02/2024 | Real Time with...IPC APEX EXPOPeter Tranitz, senior director of technology solutions at IPC, shares insights into his role as the design initiative lead. He details his advocacy work, industry support, and the responsibilities of the design initiative committee. The conversation also covers the revamping of standards, the IPC Design Competition, and the implementation of design rules in software tools.

Real Time with… IPC APEX EXPO 2024: Ventec Discusses New Pro-bond Family of Advanced Products

05/01/2024 | Real Time with...IPC APEX EXPOChris Hanson, Ventec's Global Head of IMS Technology, outlines the launch of four pro-bond formulas that deliver an outstanding combination of low dissipation factor (Df) with a dielectric constant (Dk) range to maximize the design window for critical PCB parameters. As Chris points out, Pro-bond is designed for low-loss, high-speed applications, while thermal-bond dissipates heat from a component through the board to a heat sink.

IPC's Vision for Empowering PCB Design Engineers

04/30/2024 | Robert Erickson, IPCAs architects of innovation, printed circuit board designers are tasked with translating increasingly complex concepts into tangible designs that power our modern world. IPC provides the necessary community, standards framework, and education to prepare these pioneers as they explore the boundaries of what’s possible, equipping engineers with the knowledge, skills, and resources required to thrive in an increasingly dynamic field.

On the Line With… Talks With Cadence Expert on SI/PI for PCB Designers

05/02/2024 | I-Connect007In “PCB 3.0: A New Design Methodology—SI/PI for PCB Designers,” subject matter expert Brad Griffin, Cadence Design Systems, discusses how an intelligent system design methodology can move some signal and power integrity decision-making into the physical design space, offering real-time feedback.

iNEMI Packaging Tech Topic Series: Role of EDA in Advanced Semiconductor Packaging

04/26/2024 | iNEMIAdvanced semiconductor packaging with heterogenous integration has made on-package integration of multiple chips a crucial part of finding alternatives to transistor scaling. Historically, EDA tools for front-end and back-end design have evolved separately; however, design complexity and the increased number of die-to-die or die-to-substrate interconnections has led to the need for EDA tools that can support integration of overall design planning, implementation, and system analysis in a single cockpit.